Readiness is the best policy

Readiness is the best policy

INSURANCE SOLUTIONS FOR THE HIGH NET-WORTH. TEXT BY RAOUL VILLEGAS.

A WITTY OBSERVER riffling on Benjamin Franklin’s famous aphorism said, “Yes, it is true that the only certain things are death and taxes. They forgot to add that you can only die once — and yet you can always pay more taxes.”

In death, as in life, the taxman always comes to visit. When the taxman visits, only those with astute wealth transfer strategies can ensure that the bulk of the estate goes where it is supposed to go, with a minimum of regulatory interference.

While not yet a widely known wealth-preservation-intransit transfer tactic, the use of life insurance proceeds to pay estate taxes has begun to gain acceptance. With the proper level of life insurance coverage, in death the owner of the estate can ensure that all, if not most, of the estate taxes are paid and the estate (with the proper amount of structuring) can pass cleanly to the next generation.

The reason that this tactic works comes from the concept of matched cashfl ows. When the estate owner dies, the Bureau of Internal Revenue (BIR) levies an estate tax. Consequently, there is an expectation that there will be a cash expense for estate taxes. In order to o set the anticipated estate tax, the proactive estate owner, while still alive, takes out a life insurance policy on himself, with the proceeds calibrated to closely match the expected estate taxes.

When the estate owner dies, the BIR reviews the estate documents and levies estate taxes, and the benefi ciaries (presumably the family of the estate owner) receive the proceeds from the life insurance policy, which are then paid to cover the taxes due to the BIR. The cash proceeds from the life insurance policy funds the cash expense of the estate tax. In both cases, the passing of the estate owner triggers both the levying of the estate tax, and the payment of said tax from the life insurance policy.

In order to be able to implement this tactic, the estate owner must follow four steps at regular intervals (annually if possible): 1) conduct an appraisal of the entire estate to determine approximate market values, and likely estate taxes; 2) determine the appropriate level of life insurance coverage required to cover the estimated estate taxes; 3) adjust the life insurance coverage to the proper level; and 4) pay the insurance premiums.

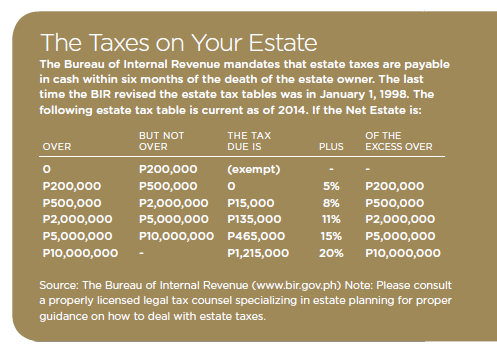

Several advantages accrue from using life insurance to cover estate taxes. First, the triggering event, the passing of the estate owner, means that estate taxes become due, but also that the proceeds of the life insurance policy are paid to the benefi ciary family — there is a certainty of cash proceeds to cover the estate taxes. Second, one pays only the life insurance premiums (a fraction of the amount) for the life insurance policy. In the event of a covered death, the fact that the insurance policy pays out substantial returns on investment compared to the original premiums paid may benefi t the benefi ciary family. Third, with variable universal life insurance products, cash value from the premium payments builds up over time. If the stock and/or bond markets perform well over time, the proceeds from a variable universal life policy can exceed the face value of the policy. Fourth, the BIR requires payment of estate taxes in cash within six months from the date of the death of the estate owner. Many families typically lack the liquidity required to settle estate taxes in such a short time frame. Having the life insurance policy act as a liquidity backstop on the estate tax, helps.

Most likely, estate taxes are not the only concern of high net-worth individuals. Transferring an estate in death is a tricky exercise, made more so with the magnitude and variety of assets owned by wealthy families.

Aside from estate preservation versus taxation, the issues faced by wealthy families regarding wealth transfer include (but are not limited to), asset identifi cation and quantification; preservation of documents and proof of ownership; maintaining control of the estate; the ability to divide the estate evenly; liquidity (a concern of asset-rich, but cash-poor families); accurate valuation (particularly real estate and other hard-to-value assets, like art); having a proper will (dying intestate introduces all sorts of complications); and avoiding confl ict among heirs.

One may surmise that tax concerns occupy only a certain subset of the issues on estate planning with which a family has to deal. It therefore becomes doubly important for a family with a substantial estate to engage the services of a professional estate-planning advisor who is knowledgeable about the law and tax issues facing estate plans.